Incoterms 2020 overview

The Incoterms 2020 are the ninth revision of Incoterms since their inception in 1936. Since their inception, Incoterms have been periodically revised and updated to keep them relevant and to adapt them to changes in international trade.

The Incoterms are now arranged in two categories as follows:

Rules for Any Mode of Transport:

- EXW – Ex Works

- FCA – Free Carrier

- CPT – Carriage Paid To

- CIP – Carriage and Insurance Paid

- DAP – Delivered At Place

- DPU – Delivered at Place Unloaded

- DDP – Delivered Duty Paid

Rules for Sea and Inland Waterway Transport Only:

- FAS – Free Alongside Ship

- FOB – Free On Board

- CFR – Cost and Freight

- CIF – Cost, Insurance and Freight

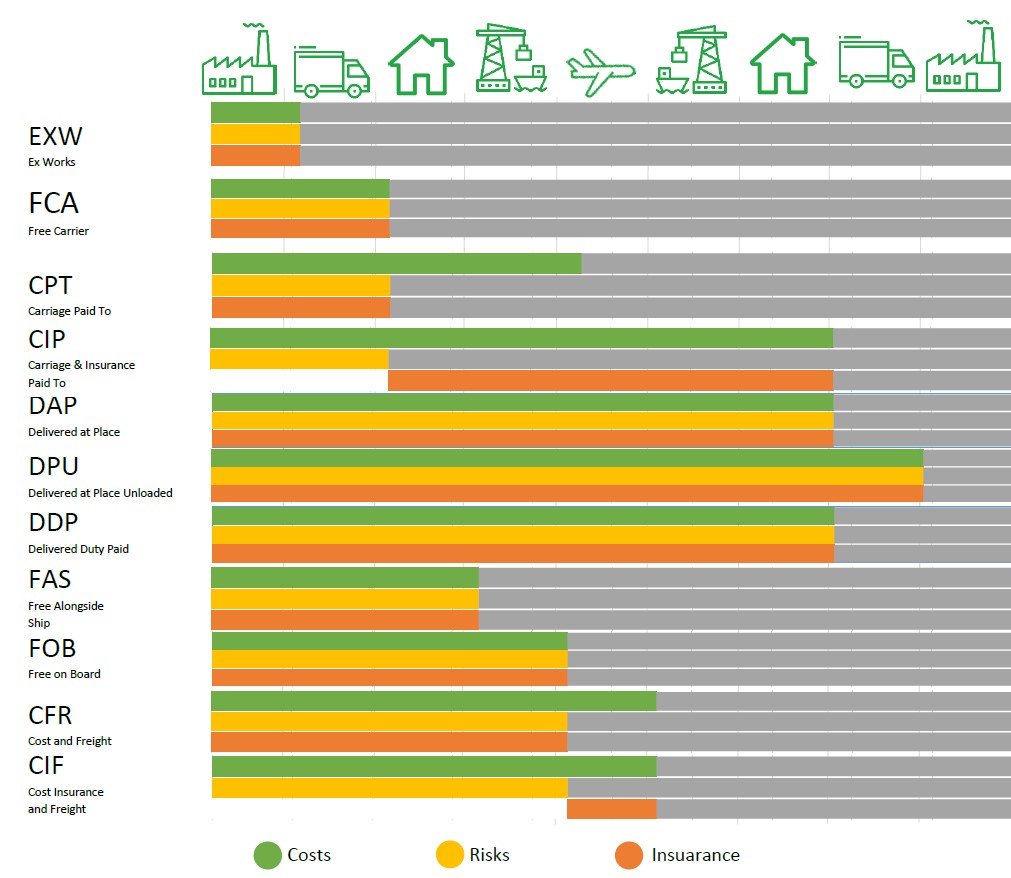

| EXW Ex Works |

The seller makes the goods available to the buyer in their own warehouse and is only responsible for packing the goods. The buyer bears all of the costs (including customs clearance and delivery) and responsibilities from the moment the goods cross the warehouse prior to loading. Risks: at the time of transfer of goods at the seller’s warehouse. |

| FCA Free Carrier |

The seller bears the costs and risks up to delivery by a carrier nominated by the buyer, including the cost of export clearance. The buyer bears the costs from loading on board to unloading, including the cost of import clearance. Risks: at the moment of transfer goods from the seller to the carrier. |

| CPT Carriage Paid To |

The seller delivers the goods and bears the costs until the goods are delivered to an agreed place, i.e., they are responsible for all of the costs at origin, export clearance, the main transport and usually costs at destination. The buyer unloades the goods and is responsible for import procedures and formalities. Risks: at the moment of transfer goods from the seller to the carrier. |

| CIP Carriage & Insurance Paid To |

The seller delivers goods and bears the costs up to delivery at an agreed place at destination, i.e., the costs at origin, export clearance, freight and also insurance which is mandatory. The buyer unloades the goods and is responsible for import procedures and formalities. Risks: at the moment of transfer goods from the seller to the carrier. |

| DAP Delivered at Place |

The seller delivers goods to an agreed place and bears all the costs and risks at origin, freight and inland transport. The buyer is only responsible for import clearance and unloading. Risks: at destination. |

| DPU Delivered at Place Unloaded |

The seller bears the costs and risks arising at origin, packing, loading, export clearance, freight, delivery at the agreed point and unloading at destination. The buyer is responsible for import clearance procedures. Risks: at destination after unloading. |

| DDP Delivered Duty Paid |

The seller bears all costs and risks from packing and checking in their warehouses to delivery at final destination, including export and import clearance, freight and insurance. The buyer only has to receive the goods and usually unloads them. Risks: at destination. |

| FAS Free Alongside Ship |

The seller delivers the goods to the port of origin loading dock and bears the costs up to delivery as well as being responsible for export customs procedures. The buyer is responsible for loading on board, stowage, freight and other costs up to delivery at destination, including import clearance. Risks: at loading dock in the port of origin. |

| FOB Free on Board |

The seller bears the costs until the goods are loaded onto the ship, including export clearance. The buyer is responsible for the cost of freight, unloading, import clearance and delivery at destination. Risks: on board after loading. |

| CFR Cost and Freight |

The seller is responsible for all costs until the goods arrive at the destination port, including export clearance, costs at origin and freight. The buyer is responsible for unloading, import procedures and transport to destination. Risks: from the moment the goods are on board. |

| CIF Cost Insurance and Freight |

The seller is responsible for all costs until the goods arrive at the destination port, including export clearance, costs at origin, freight and insuarance which is mandatory. The buyer is responsible for unloading, import procedures and transport to destination. Risks: from the moment of full loading on board. |